Geopolitical shocks are not point events. A sanctioned sovereign, a closed strait, a defaulting frontier economy — each transmits through the trade, capital and security ties that bind countries together, and the damage to a portfolio is rarely where the headline lands. Pricing that requires more than a dashboard of country scores; it requires a model of the network. Simudyne’s geopolitical risk platform is exactly that: a high-fidelity, agent-based simulation in which heterogeneous country agents, coupled by real economic and financial linkages, generate forward-looking risk from the bottom up.

Monitor the signal. Simulate how it propagates across the network. Price the move before it is fully in.

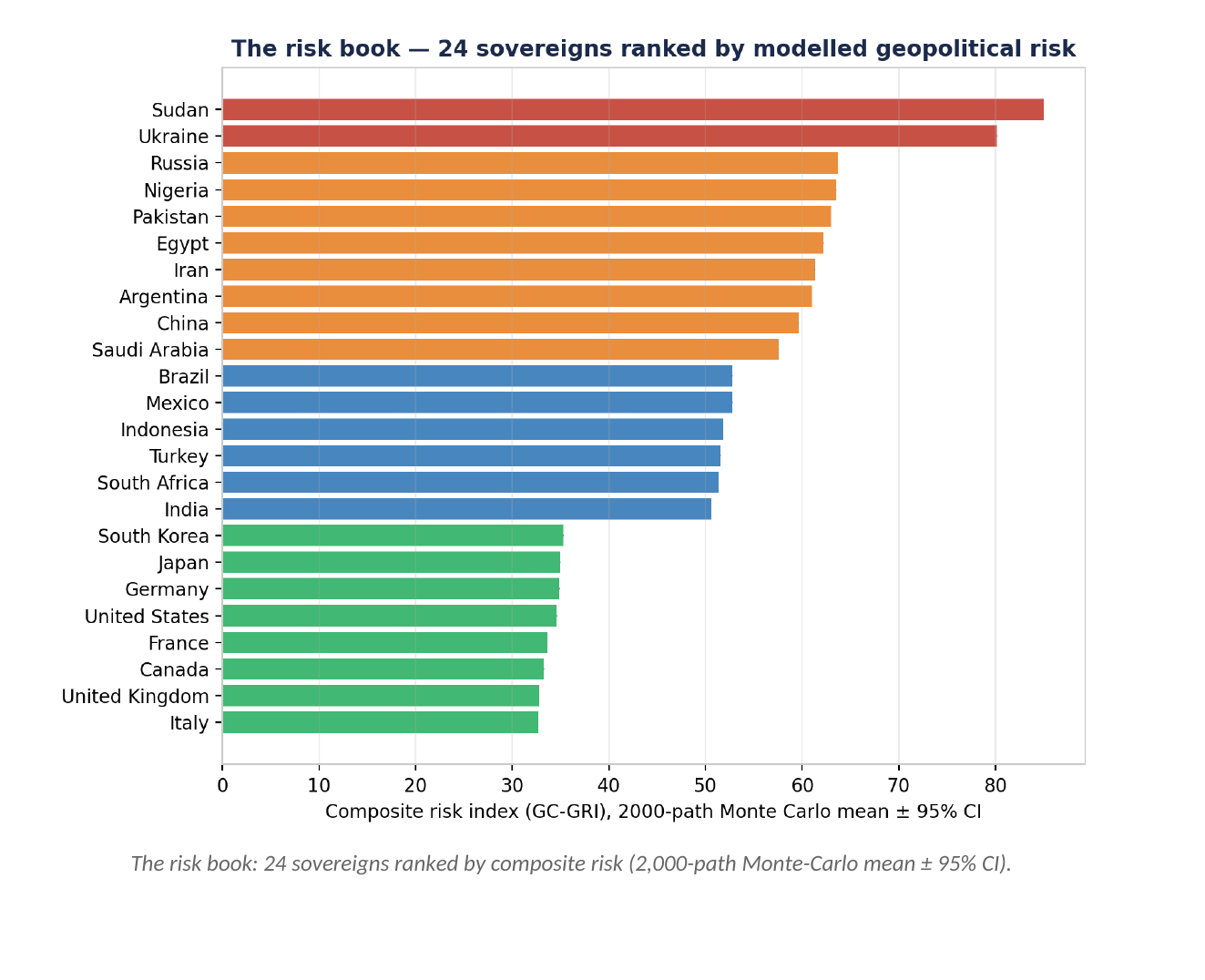

A risk book ranked by what matters

Every country is an agent described by twenty-five indicators across five pillars — political, external, economic, social and environmental — grounded in recognised public data and combined into a composite Geopolitical Country Risk Index (GC-GRI). Run as a Monte-Carlo ensemble, the platform produces a risk book that orders sovereigns the way a macro desk would, with fragile and conflict states at the top and deep, well-governed economies at the bottom.

| Tier | GC-GRI | Profile |

|---|---|---|

| Sudan | 85 | Civil war, displacement, fiscal collapse |

| Ukraine | 79 | Active war, financing strain |

| Russia | 64 | Sanctions, war footing, governance stress |

| Nigeria · Pakistan | ≈63 | Frontier fragility, FX and security stress |

| Germany · UK · Canada | 33–40 | Strong institutions, deep capital markets |

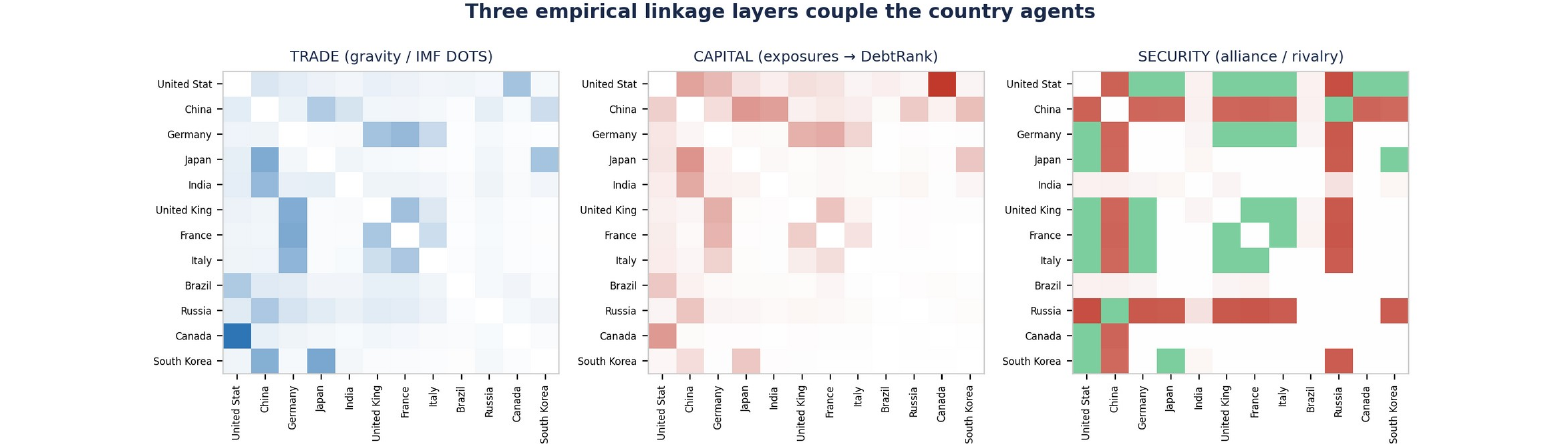

Shocks travel real linkages — not a single graph

The core of the model is its network. Countries are coupled by three distinct, empirically-grounded layers: a trade layer built from a gravity model and IMF Direction of Trade Statistics; a capital layer of cross-border exposures; and a signed security layer of alliances and rivalries. A shock travels each channel on its own terms — demand contracts along trade ties, distress spreads along exposures, conflict escalates along rivalries — so the propagation is structural, not a one-size-fits-all diffusion.

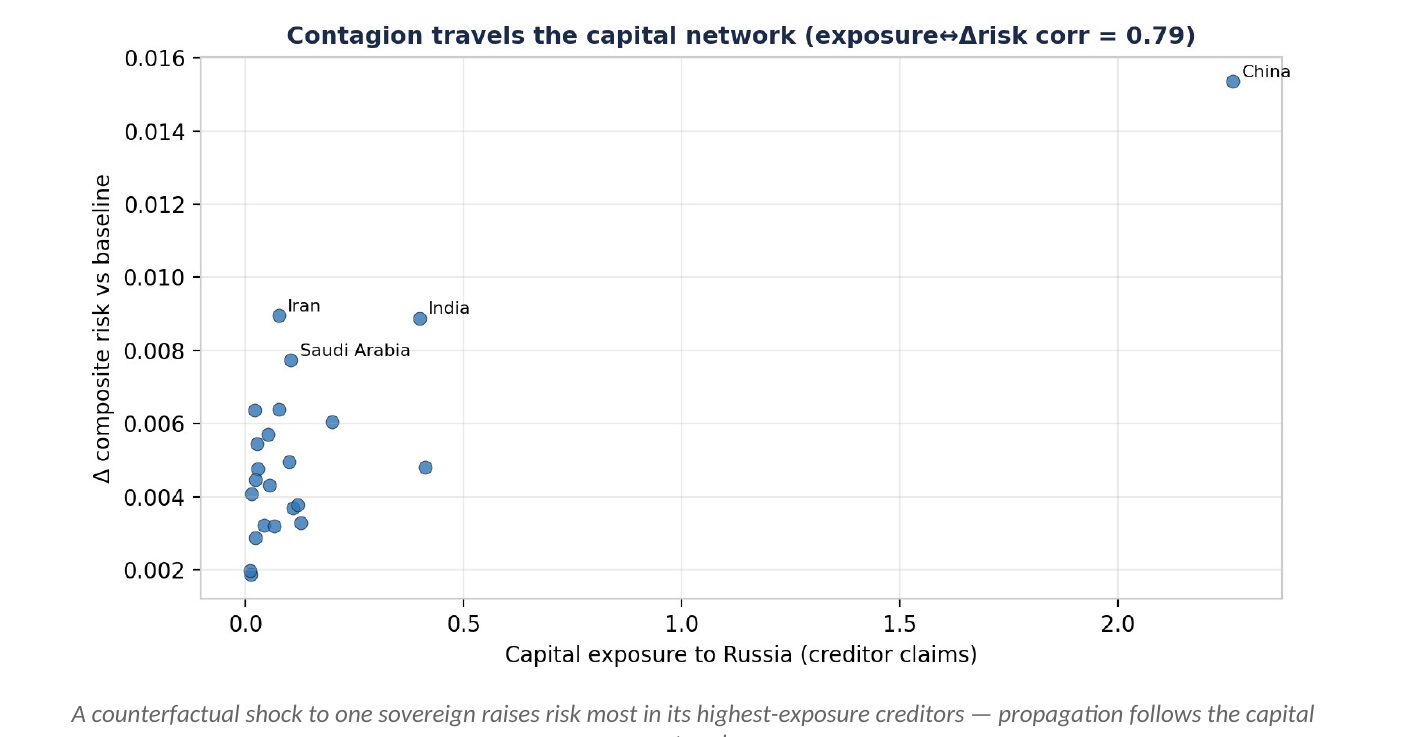

Contagion you can trace

On the capital layer the platform runs a DebtRank clearing pass — the systemic-risk algorithm used in central-bank stress analysis — iterated to convergence each month. When a sovereign’s equity is impaired, its distress propagates to creditors in proportion to their exposure. The effect is measurable and directional: in a counterfactual shock to Russia, the countries whose risk rises most are precisely its largest creditors, with an exposure-to-impact correlation near 0.8

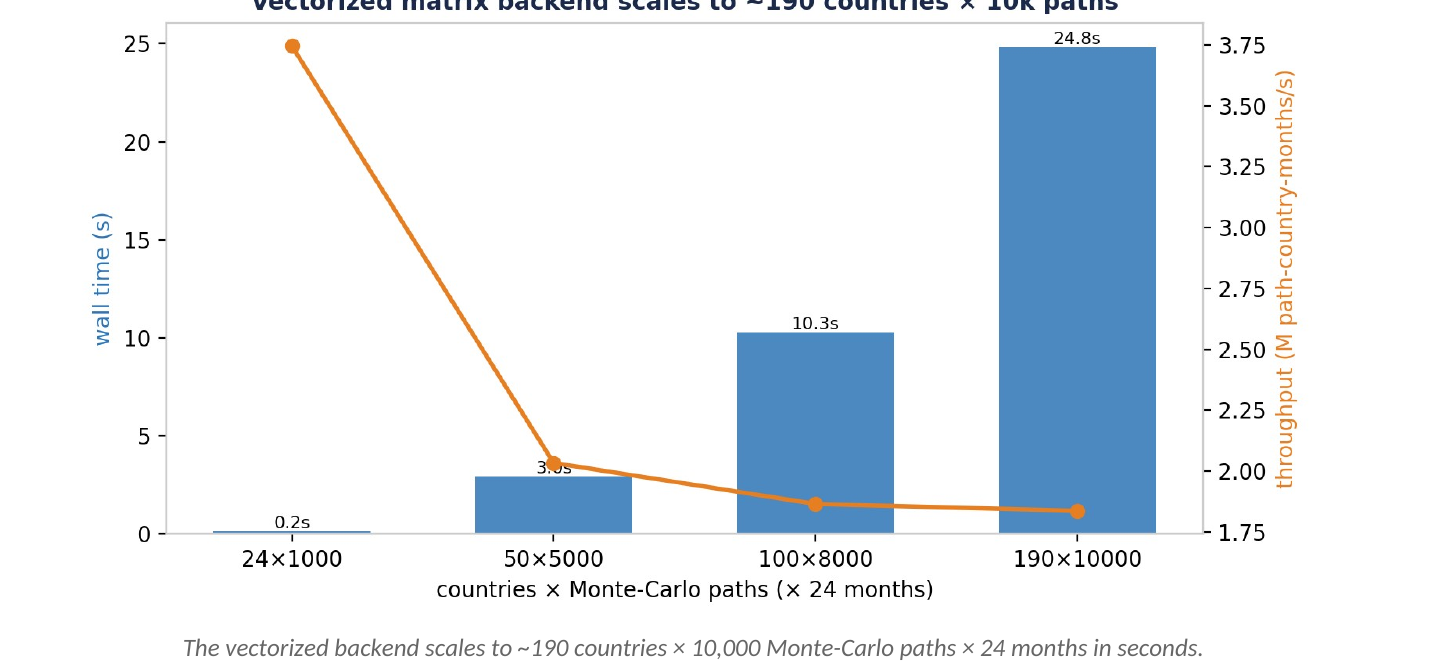

Calibrated by live data, built to scale

The same data loop that scores the live book also calibrates the scenarios stressed against it: news-attention scores set shock probabilities, market-implied moves set magnitudes, and the trade network is refreshed from IMF DOTS. And because the engine is a vectorized matrix backend — every Monte-Carlo path advances simultaneously — it stresses roughly 190 countries over thousands of paths in seconds, with every run seeded and reproducible

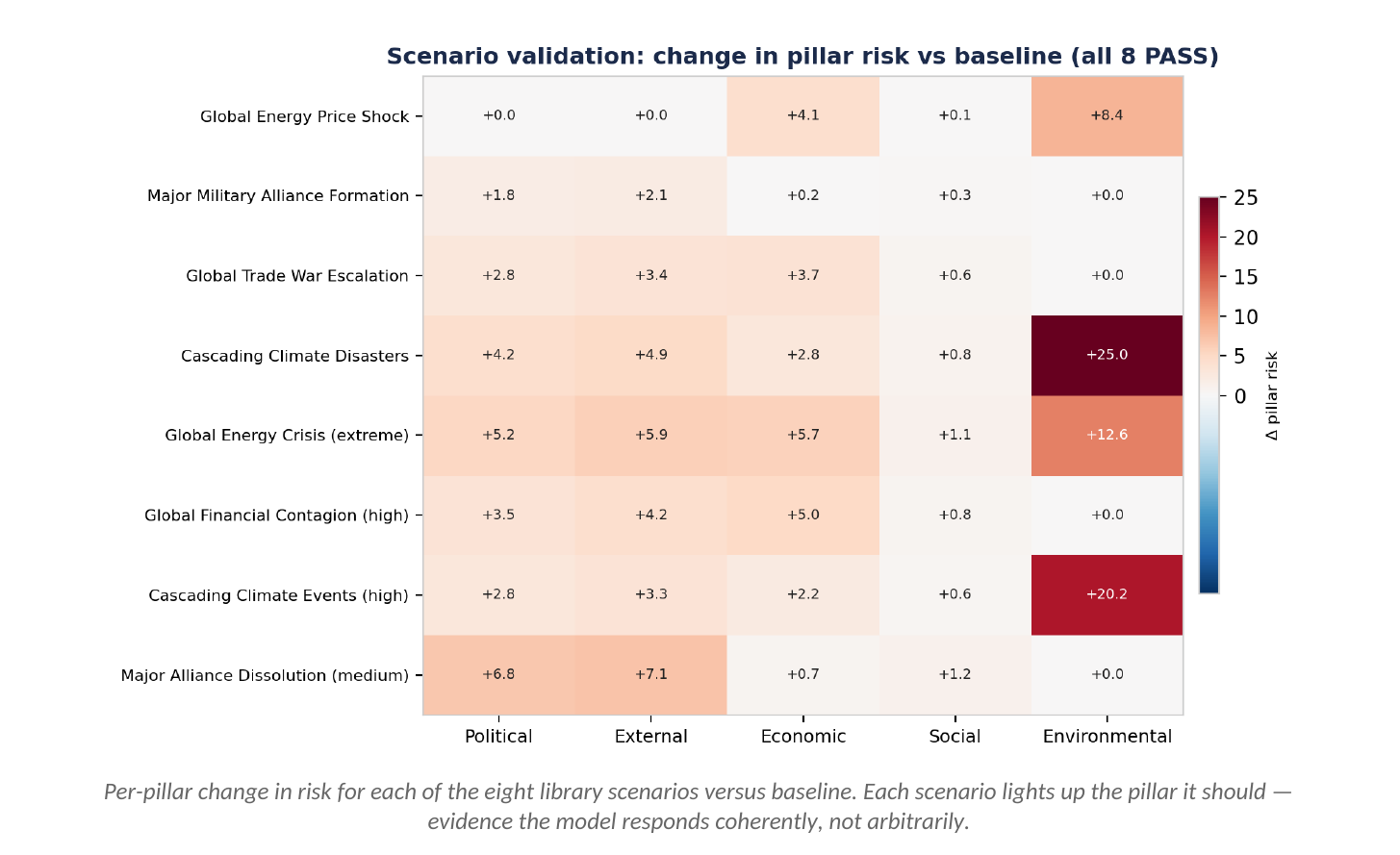

Validated against its own scenarios

Before trusting a model to price shocks, you check that it does what it claims. We ran all eight scenarios shipped in the platform’s Scenario Builder and Stress Test Runner — energy shocks, trade wars, financial contagion, cascading climate disasters, alliance shifts — through the engine, comparing each against a baseline and decomposing the response by risk pillar. Every one of the eight moved the book in the right direction and, crucially, raised the right pillar: energy and trade shocks hit the economic pillar, climate scenarios the environmental pillar, alliance shocks the political and external pillars. Eight out of eight validated, with reproducible results

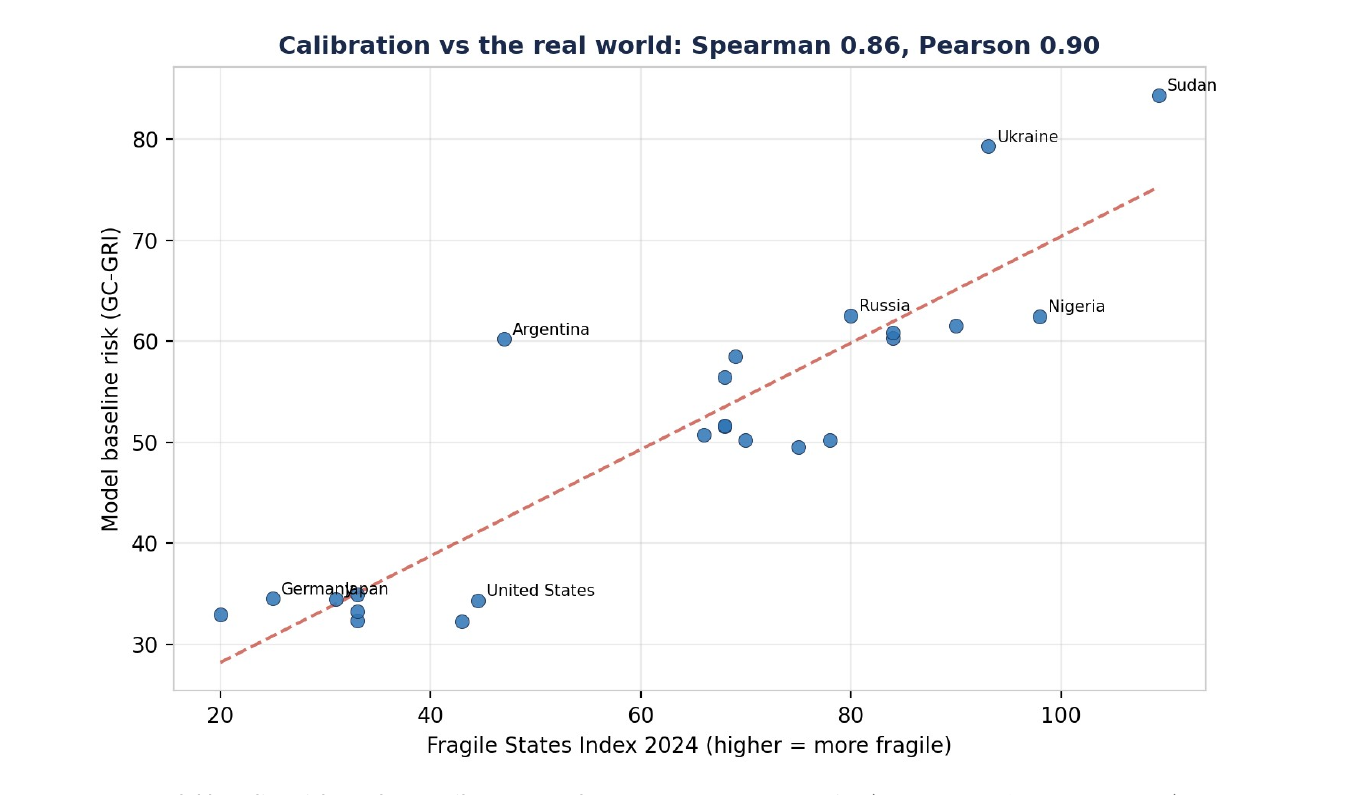

Backtested against history

The harder test is whether the model matches the real world. Run blind, its baseline country ranking correlates with the Fund for Peace Fragile States Index 2024 at a Spearman rank correlation of 0.86 — it independently places Sudan, Ukraine, Nigeria and Pakistan at the top and Germany, Japan and Canada at the bottom, the same ordering a recognised fragility index produces

Event reproduction is more mixed — and the misses are the most useful part. We replayed five documented episodes and scored whether the model raised risk in the countries actually affected:

| Historical episode | What we checked | Result |

|---|---|---|

| 2014 Crimea | Top-2 affected = Russia, Ukraine | 1.00 — reproduced |

| 2022 Russia–Ukraine | Russia & Ukraine spike hardest | 0.67 — reproduced |

| 2020 COVID (global shock) | Broad rise across the book | 96% of countries up |

| 2008 Financial Crisis | Contagion to major creditors | Mechanism right (corr 0.81), needs real exposures |

| 2018 EM FX crisis | Worst in Argentina/Turkey | Partial — saturation effect |

Conflict events reproduce cleanly, and a global shock raises the whole book as it should. The two partial results are honest and instructive rather than embarrassing: in 2008 the contagion mechanism works — distress travels in proportion to exposure (correlation 0.81) — but the capital network is currently inferred from trade rather than real cross-border bank claims, so it flags the wrong creditors; supplying a BIS/CPIS exposure feed fixes it without touching the model. And already-distressed economies like Argentina sit near the top of a bounded scale, so a fresh shock has little room to move them. We chose to report these plainly rather than tune them away — a model you can trust is one whose limits are documented, not hidden.

Why this matters for an asset manager

Together these turn geopolitical narrative into something a CIO, risk officer or macro strategist can size a position on:

- Networked, not nodal — Risk is priced across real trade, capital and security linkages, so a shock in one country shows up where it actually transmits, not just where it started.

- Contagion you can trace — A DebtRank capital-clearing pass quantifies which creditors inherit a distressed sovereign’s stress — second-order P&L, ex-ante.

- Calibrated by live data — The trade layer is built from IMF Direction of Trade Statistics; attention and market-implied signals set shock probabilities and magnitudes.

- Built for the desk — Thousands of reproducible Monte-Carlo paths across ~190 countries in seconds, every run seeded and auditable for risk and compliance.

The pay-off is the same one the desk has always wanted from geopolitics and rarely gets: a defensible, forward-looking estimate of what a shock does to the book — across the whole network — before the move is fully priced.

🔗 Live Demo — Try the Platform Now

A high-fidelity agent-based platform that turns live signals into portfolio decisions

🔗 Download the Whitepaper

An Agent-Based Model of Geopolitical Risk: Agents, Multi-Layer Linkages, and Network Contagion

About Simudyne

Simudyne builds agent-based simulation technology that helps financial institutions model complex, emergent risk from the bottom up — from climate-financial stress testing to market microstructure and geopolitical risk. The platform simulates how shocks propagate through portfolios and the wider system, with the reproducibility and documentation that risk and compliance functions require.

See it on your book — simudyne.com